T&M House

Case exhibits

2 exhibits for this case

TMHouse-exhibit-3

Suggested case structure

1. Context

1. How would you calculate capacity utilisation for the client?

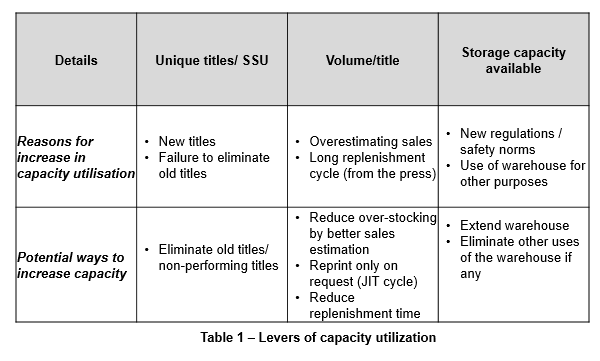

- Unique titles: The number of unique titles that the warehouse stocks woud impact the capacity utilisation. Each title has a specific storage unit (SSU) which is the amount of space required (in cubic centimeters) to store that title.

- Volume per title: The number of units or volume per title would impact the capacity utilisation.

- Storage capacity available: The amount of storage space available after accounting for safety regulations/ other spaces etc. would also be a key determinant of capacity utilisation.

Below would be the formula for capacity utilisation:

Capacity utilisation = (SSU x Volume)/ Available capacity

2. What could be the reasons for the warehouse to reach its maximum capacity? What are the potential levers to increase the capacity?

- Increase in unique titles: The increase in the number SSU's stocked either due to the addition of new titles or failure to destroy/ dispose the older titles could be one reason for higher capacity utilisation.

- Increase in the volume per title: Overestimating potential sales or longer replenishment cycle of books from the press could lead to an increase in the volume stocked per title which in turn will impact capacity utilisation.

- Reduction in storage capacity available: A reduction in the storage capacity available would also lead to higher utilisation. This could be due to new regulations / safety norms or usage of space for other purposes.

- Reduce unique titles: Elimination of titles which are old/ not performing may help increase available capacity.

- Decrease the volume per title: This would be a key lever to increase available capacity. This can be achieved in several ways - reducing initial stock per title, estimating sales better, reprinting books only on request, shorten replenishment cycle from the printing press etc.

- Increase the storage capacity available: The capacity can be increased by extending the warehouse or by eliminating usage of the warehouse for other purposes (if any).

Share the following information with the interviewee if enquired:

- There have been no new titles added recently by the client

- The company also provides storage services to other small publishing houses. This accounts for 50% of the warehouses's flow. The company stores the books, packages and ships them out to the retailers on the request of the publisher

- The company charges the other publishers for this service. The company is not tied up in a long term contract with these publishers, so it would be possible to terminate these agreements at a 3 month notice if required.

- An option to increase the available capacity would be to terminate some or all of the agreements with third party publishers and free up space.

3. What factors should the company consider while choosing the publishers whose contracts should be terminated?

The objective of terminating the publisher would be two fold - maximising the space freed up and minimising impact on revenue (fee charged for storage). This has the underlying assumption that the profits made on our own books is more than 5% (which seems reasonable).

Below would be the key considerations for choosing a publisher:

- Maximising space freed up - publishers who have bulky titles (SSU is high)

- Minimising revenue impact - publishers who have low average price

2. Cost analysis

4. Can you help evaluate the impact of terminating a publisher contract on the P&L of the firm?

The P&L impact would be equal to the loss of revenue minus the reduction in costs.

- Revenue loss would be a function of the average price of the books stored and the volume stored. This would reduce if a publisher is terminated.

- The fixed costs would remain constant - warehouse maintenance, admin staff, IT, etc.

- The variable costs would include packaging material, handling personnel etc. These costs are likely to reduce if a publisher is terminated.

5. Can you identify the drivers of the variable costs of the company?

There are two key variable costs - handling staff and packaging material. The potential drivers of these costs could be:

- Handling staff - The number of times the books are replenished (from the press) or shipped out to the retailers would determine the costs assosciated with handling staff

- Packaging material - The SSU and the associated volume would determine the packaging material required when the books are shipped out to the retailers

3. Options

6. The company has identified Publisher X as the potential publisher whose contract should be terminated. The company has estimated that the space freed up by this termination would be sufficient to tide over the capacity challenge in the foreseeable future. Can you calculate the impact of the termination of Publisher X on the profits of the firm?

Share the following information with the interviewee if enquired:

- We know the following details about the publisher. Publisher X accounts for:

- 10% of the total revenue

- 20% of the volumes stocked in the warehouse

- 15% of the order lines in the warehouse

- The volumes stocked in the warehouse have a direct impact on the packaging costs.

- Order lines are a function of the number of times the books need to be handled during replenishment or outward shipping. This has a direct impact on the handling staff costs.

- The current margin of the warehouse is $ 5 m and the margin percentage is 25%

Using the above information, the following can be calculated:

Total Revenue = Margin / Margin % = $ 5m/ 25% = $ 20 m

Total Costs = Revenue - Margin = $ 20 m - $ 5 m = $ 15 m

Using the cost structure shared earlier, the different cost components can be calculated:

Handling staff cost = Costs x 40% = $ 15 m x 40% = $ 6 m

Admin / IT staff cost = Costs x 20% = $ 15 m x 20% = $ 3 m

Packaging cost = Costs x 20% = $ 15 m x 20% = $ 3 m

Maintenance cost = Costs x 10% = $ 15 m x 10% = $ 1.5 m

Depreciation = Costs x 10% = $ 15 m x 10% = $ 1.5 m

Termination of Publisher X would only impact the handling costs, packaging costs and the revenue:

New handling staff cost = Earlier Costs x (1- 15%) = $ 6 m x 85% = $ 5.1 m

New packaging cost = Earlier Costs x (1- 20%) = $ 3 m x 80% = $ 2.4 m

New total cost = $ 5.1 m + $ 3 m + $ 2.4 m + $ 1.5 m + $ 1.5 m = $ 13.5 m

New revenue = Earlier Revenue x (1-10%) = $ 20 m x 90% = $ 18 m

New margin = $ 18 m - $ 13.5 m = $ 4.5 m

Net impact on P& L = Earlier Margin - New Margin = $ 5 m - $ 4.5 m = $ 0.5 m

4. Conclusion

7. Now that we know the economic impact of terminating Publisher X, what would you recommend to the client - termination of Publisher X or investing in the extension of the warehouse?

There are two choices before the client : Invest $ 10 m now to increase warehouse capacity or terminate Publisher X which would impact the P&L by $ 0.5 m every year.

Assuming that all other factors remain the same and ignoring the time value of money, a break-even point/ time period can be calculated:

Break-even point = $ 10 m / $ 0.5 m = 20 years

In other words, it would be 20 years before the yearly impact on P&L from the termination adds up to the upfront cost required to increase the warehouse capacity. Additionally, we know that the capacity freed up by the termination of Publisher X is sufficient to manage the storage needs in the foreseeable future.

Based on this analysis, the client should not invest in the capacity extension of the warehouse. They should instead terminate the storage contract with Publisher X in order to increase the available capacity.